Much has been said about inflation hurting society. As people’s buying power decreases, life gets more costly. Heck, the Fed seems hell-bent on causing another recession to contain inflation.

However, as I look at the historical price changes of some of our most important consumer goods and services, I can’t help but think combatting inflation is straightforward.

Further, for the average household, perhaps the negatives of inflation are overblown. Sure, we all know food, gas, and utility prices are higher. However, these costs are counteracted by higher wages as well.

Other than these three recurring items, inflation doesn’t seem that bad. Further, these three items don’t make up a large portion of my overall budget. Do they for you?

Let’s first take a look at an inflation chart of various goods and services to understand how prices have changed.

Inflation Of Various Consumer Goods And Services

Check out this great inflation chart by Visual Capitalist.

Since 2000, the following consumer goods and services have risen the most in price:

- Hospital Services

- College Tuition and Fees

- College Textbooks

- Medical Care Services

- Childcare

- Food and Beverage

- Housing

- New Cars

- Household Furnishings

Since 2000 the following consumer goods and services have declined the most in price:

- Televisions

- Toys

- Software

- Cellphone Services

- Clothing

Straightforward Solutions To Combatting Inflation

It’s likely the price change trends for the items above will continue for the foreseeable future. Therefore, the straightforward solutions to combatting inflation are to:

- Not go to college

- Attend community college or a state college

- Stay in great physical and mental shape to decrease your chances of receiving medical services

- Eat less and / or substitute cheaper foods

- Don’t buy a new car because the average new car price is absurd

- Drive your existing car for as long as possible

- Not have kids or have fewer kids

- Buy a house with a fixed-rate mortgage

- Own stocks (S&P 500) and other risk assets that tend to increase in price faster than inflation

Pretty simple right?

Get Richer From Inflation Instead

If you do the above, you likely won’t feel the negative effects of inflation as much if at all. Instead, you will likely feel good about inflation because your income is likely inflating at a similar or faster rate.

Inflation generally acts as a tailwind for real estate owners as it helps push rents and property prices higher, while mortgage rates stay fixed.

Inflation also tends to boost corporate profits as companies can often charge more for goods and services faster than their increase in expenses.

So long as you are working in a competitive industry and investing most of your cash in risk assets that have historically beaten inflation, you’ll likely end up wealthier with the help of inflation.

But Counteracting Inflation Is Not Easy

Of course, not all of you will completely agree with all the above-listed items to combat inflation.

I suspect some of you may balk at not going to college, going to a state school (the horror!), eating less, and not having kids the most. Further, if you have kids already, it’s not like you can just return them!

Hence, let’s discuss these items in a little more detail. Everybody has different opinions. We must weigh the costs and benefits of each compared to the clear benefits of saving money.

The more you desire to save money, the more you will agree with the solutions and vice versa.

Defeat Inflation By Not Going To College

Nowadays, paying full college tuition truly feels like a ripoff. When everything can now be learned for free online or be learned from reading great books, it’s baffling why going to college still costs so much.

Plenty of students are going to college for four years and paying six figures for tuition only to graduate with no job or a job that doesn’t require a college degree. Being overeducated and underemployed are terrible for your finances. The danger in paying full freight to go to college has never been higher!

As a public college graduate, I’m telling you things will be OK if you choose to go the less expensive route. The key is to network and be aggressive when applying for various opportunities to get your foot in the door. Once you’re in, nobody cares where you went to college. People care about performance.

Yes, college graduates tend to earn more over their lifetimes than do those who only went to high school. However, please be sensible about the amount of time and money you are willing to spend to go to college. The internet makes learning far quicker than 30 years ago. Yet, it still takes four years for the average person to get a degree.

Take Advantage Of Online Resources

One of the main reasons why I consistently write on Financial Samurai is to offer free personal finance education to anyone who wants to learn.

I also firmly believe if you read Buy This, Not That and subscribe to my weekly newsletter, you will have more financial knowledge than 99% of the population.

Of course, I’m biased. However, I’ve got the experience and the bank account to back up my beliefs. Then there is the plethora of free online courses (MOOC) from plenty of major universities as well. Take advantage.

Unless your family is already rich, it may be better to skip college and pay directly for courses you want to specialize in. For example, you can go to a coding boot camp where you only pay after you get hired. Or you can become an apprentice to someone in the vocational trades.

Teach Your Kids Everything You Know

I asked my son what he learned the other day. And he told me about some things he had learned two years earlier when we homeschooled him.

This was when I realized all we parents have to do is teach our children everything we know! If our kids learn everything we know, then they might be able to do what we do for a living.

If we are college graduates, there’s actually no need to spend $500,000 on college ten years from now if we spend time teaching them. We just have to dedicate more time to them.

As a graduate of The College of William & Mary, a liberal arts school, I should be able to teach my kids everything from history to Mandarin. As a graduate of UC Berkeley’s Haas School of Business, I should be able to teach them about cash flow statements, marketing, and organization behavior.

If we are unable to teach our children anything we learned, did we really learn anything? In a meritocracy, we need to teach useful skills.

Eat Less, Don’t Waste Food, Stay In Better Shape

I’m not sure why these recommendations to counteract inflation may be controversial. Surely, eating less will save you money. Staying in better shape will increase your chances of living a more comfortable and longer life.

Once we learned in 2020 that the people who died the most from COVID-19 had the most comorbidities, most of us decided to exercise more and eat healthier. We rationally feared dying earlier from a virus, so we collectively did something to improve our odds of surviving.

Unfortunately, American health care is outrageously expensive. We spend the most per capita yet do not have the highest life expectancy in the world.

If the rising cost of food is unbearable, we will eat cheaper foods and ration our food more carefully. We also won’t waste as much food.

According to FeedingAmerica.org, each year, 119 billion pounds of food is wasted in the United States. That equates to 130 billion meals and more than $408 billion in food thrown away each year. Shockingly, nearly 40% of all food in America is wasted.

Food waste in our homes makes up about 39% of all food waste – about 42 billion pounds of food waste. Let’s say 16% of our food gets tossed in the trash every week. If we ate 100% of the food we purchased a year, we would easily counteract 16% annual food inflation.

Saving Money By Not Having Kids

Not having kids is a non-starter for many folks who want kids.

But if you don’t have kids, you won’t have to save for their college tuition, pay for childcare, buy college textbooks, get as big of a house, get as large of a car, buy as much food, buy as many plane tickets, and pay as much in healthcare expenses!

Not having kids is one of the best ways to combat inflation. You can’t purposefully decide to have a lot of kids then be upset by how much they cost.

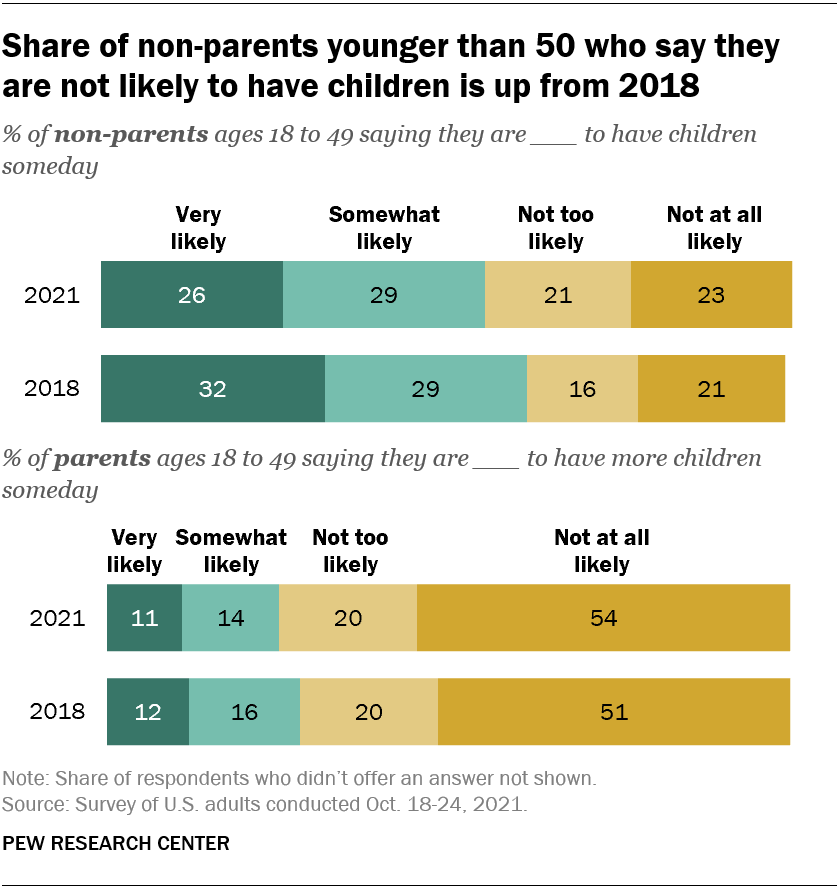

According to Pew Research, some 44% of non-parents ages 18 to 49 say it is not too or not at all likely that they will have children someday, an increase of 7 percentage points from the 37% who said the same in a 2018 survey.

Meanwhile, 74% of adults younger than 50 who are already parents say they are unlikely to have more kids, virtually unchanged since 2018. 17% of respondents say that won’t be having kids for financial reasons.

If such a large percentage of the child-bearing population is deciding not to have kids or not to have more kids, then inflation may not be as insidious in society as we think.

Life Is Pretty Affordable Without Kids

Without kids, our cash flow would be much higher.

First, we wouldn’t have bought another house 2020. The 1,920 square feet, three bedroom, two bathroom house we bought in 2014 would have been plenty for the two of us. We had already downsized in cost by about 40% from the house we lived in from 2005 – 2014.

Second, we wouldn’t have all these childcare, preschool, and kindergarten expenses. Preschool in San Francisco costs $2,000 – $2,500. If we keep both kids in language immersion school, our annual tuition expense will be about $96,000 a year after taxes. I should just teach my kids Mandarin and move to Taiwan!

Third, our monthly healthcare premiums would likely be about $500 cheaper. We currently pay $2,300 a month for a family of four.

Fourth, I may have kept our Honda Fit that I leased for $225/month. I loved Rhino because he could fit in 20% more parking spots. Instead, we bought a safer car for about $60,000 after taxes. The Honda Fit’s crumple zone was tiny and it felt like the doors were made of cardboard.

Retiring early with kids is at least three times harder than retiring early without kids. I clearly understand why many parents try to work until after their kids graduate from college. The costs keep on coming.

Thankfully, most parents love their kids so much that the added costs of having them feel worth it. But that doesn’t mean parents won’t complain how expensive kids are.

Life Sometimes Feels Cheaper When Inflation Is High

During the bull market, life felt cheaper because our investments were rising far greater than our costs. When the bear market hit in 2022, we obviously felt the opposite way. Eventually, risk assets will start appreciating again, making living with high inflation easier.

Besides not having children or having fewer children, owning our primary residence is probably the easiest way to combat inflation. Once you have your living costs fixed, everything else doesn’t seem as painful.

We have options to reduce our household burn. We don’t have to send our kids to private schools. Instead of taking an Uber home, we can take a bus. There’s no need to eat a $78 dry-aged rib-eye when a $10 cheeseburger tastes just as good.

So long as we are regularly investing our cash flow, fixing our largest expenses, and living within our means, we should be net beneficiaries of inflation.

As I said, combatting inflation is straightforward. But due to human nature, keeping our costs down is not easy.

Reader Questions And Suggestions

Is inflation materially affecting your spending habits? How are you combatting inflation, if at all? What are some of the easiest things most people can do to keep costs down?

Pick up a copy of Buy This, Not That, my instant Wall Street Journal bestseller. The book helps you make more optimal investment decisions so you can live a better, more fulfilling life.

For more nuanced personal finance content, join 55,000+ others and sign up for the free Financial Samurai newsletter and posts via e-mail.

Listen and subscribe to the Financial Samurai podcast on Apple, Google, and Spotify. Financial Samurai is one of the largest independently-owned personal finance sites that started in 2009.

{kind=link}