‘Julia can resolve her debt issues,’ skilled says. ‘The complexity of the method can be rewarded with a reliable retirement earnings’

Critiques and suggestions are unbiased and merchandise are independently chosen. Postmedia could earn an affiliate fee from purchases made by means of hyperlinks on this web page.

Article content material

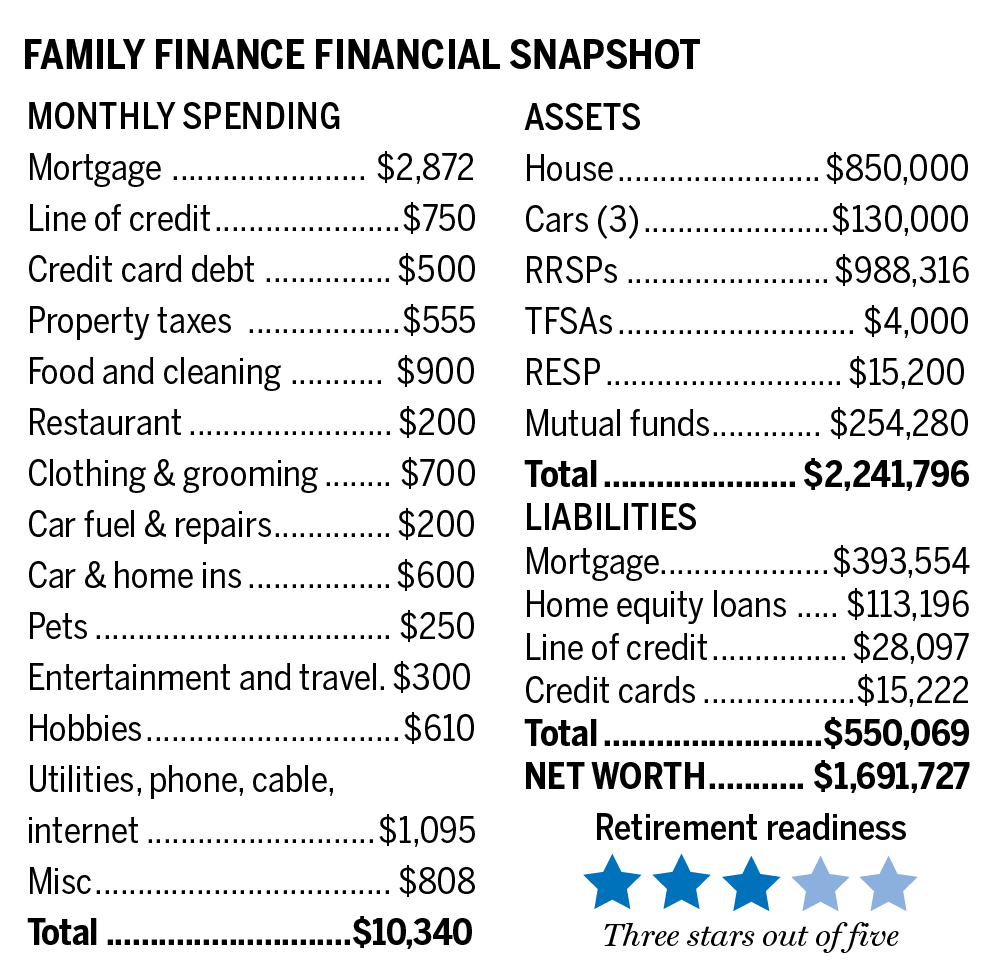

A lady we’ll name Julia, 58, lives in Alberta. Her take-home earnings works out to $10,340 per 30 days. She has one youngster of their early 20s dwelling at house and supplies a automobile and different advantages to a different of their mid-20s. Julia receives $6,000 in annual youngster help whereas the youthful lives together with her.

Commercial 2

Article content material

Julia want to retire in two years — if she will be able to afford it. Her belongings are substantial: She has an $850,000 home and $1,261,796 in monetary belongings composed of RRSPs, mutual funds and small TFSA and RESPs. If she begins her retirement at 60, these monetary belongings, excluding the RESP funds, can be sufficient to generate $56,325 per 12 months for 35 years in the event that they proceed to develop at three per cent above inflation. Julia, who works for a big vitality firm as a chemist, additionally expects a $45,000 annual defined-benefit pension, that means that she is place proper now to to gather near $100,000 in pre-tax earnings throughout her retirement.

Article content material

E-mail [email protected] for a free Household Finance evaluation

Whereas that is a superb basis, there are some causes for concern. Julia nonetheless has vital money owed together with a $393,554 mortgage, $113,196 in home-equity loans and $15,222 of credit-card debt with annual rates of interest as excessive as 19.9 per cent. She pays $2,872 per 30 days or $34,464 per 12 months on her mortgage. That’s 28 per cent of her take-home earnings.

Commercial 3

Article content material

She has tried to take cost of her affairs, however the price of carrying debt and supporting her household are weighing on her. Will she be capable to retire at 60 and maintain her house?

Discovering an answer

Household Finance requested Eliott Einarson, a monetary planner who heads the Winnipeg workplace of Ottawa-based Exponent Funding Administration Inc., to work with Julia. His plan — promote the $850,000 home and repay the whole $506,750 mortgage and residential fairness mortgage. With out the $3,622 month-to-month price of paying the mortgage and loans apart from her bank cards, she would wish to exchange solely $6,718 month-to-month earnings in retirement, Einarson estimates. That’s one thing that’s nicely inside attain.

If she cuts the youngsters’ cords of monetary dependence, she might cut back $700 per 30 days for clothes and grooming, $900 per 30 days for meals and $1,095 per 30 days for utilities, youngsters’s cell telephones and net companies and automobile insurance coverage. Underneath phrases of her separation settlement, $500 of kid help would finish. However it’s an excellent monetary tradeoff. Her month-to-month prices would go all the way down to about $5,000.

Commercial 4

Article content material

The selection is to maintain the large home and stay in debt or downsize, repay money owed, and retire with monetary safety. Her $850,000 home would carry an estimated $807,500 after 5 per cent prices. Paying off her mortgage and line of credit score would go away her with $300,750 for a hefty down cost and even outright buy of a townhouse or rental house in bustling Calgary or elsewhere within the province.

She will be able to additionally use her annual $23,000 job bonus to repay $15,222 of bank card debt, Einarson suggests.

Retirement plans

Two years from now, her DB pension will present payouts of $45,000 per 12 months. Her RRSP could have grown to $1,048,504 with no additional contributions and, with three per cent annual development after inflation, will be capable to generate $47,375 per 12 months for the next 35 years to her age 95. Her $254,280 of mutual funds with no additional additions would develop to $269,727 after which pay $12,187 for the next 35 years. That’s $104,562 per 12 months earlier than CPP or OAS begin. After 25 per cent common tax, she would have $78,421 to spend every year. That works out to $6,535 per 30 days. That’s greater than her estimated price of dwelling together with her grownup youngsters moved out.

Commercial 5

Article content material

At 65, she might add CPP at $13,000 per 12 months and OAS at present charge of $7,707 per 12 months for a complete of $125,269 per 12 months earlier than 27 per cent common tax. There can be OAS clawback at 15 per cent of earnings over $79,845 — that’s about of about $6,800. After common tax and clawback, she would have $86,646 to spend per 12 months or $7,053 to spend every month. That may cowl estimated bills and go away cash for journey or sudden bills. Even for items to her youngsters.

-

This thirtysomething couple with $390,000 in net worth has decades to save

-

Spectre of inflation adds to early retirement risk for this young B.C. couple

-

This couple wants to retire at 60, but needs to speed up their savings to get there

Beginning CPP at 60 would price her 36 per cent of the $13,000 full annual payout, so it’s price ready to 65. In any other case, over 35 years, she can be forgoing nearly $200,000. She would even be slashing the bottom for annual inflation will increase in CPP payouts. Some economies in spending — maybe charging her youngster hire — are preferable to this price, Einarson notes.

Commercial 6

Article content material

Whichever route she goes, Julia ought to attempt to elevate returns from her monetary belongings. She has left administration of investments to others and never monitored what her advisors’ recommendation does for her. Her belongings are fully in mutual funds bought by a chartered financial institution. She is unaware of the charges, how they’re charged and, certainly, why she has the current mixture of funds. To say the least, taking an energetic curiosity in her cash and maybe discovering an advisor that doesn’t promote merchandise however merely provides recommendation could possibly be to her benefit. At her $1-million-plus asset stage, she would possibly pay advisory charges of only one per cent of belongings beneath administration. On high of index fund charges of 10 to 30 foundation factors, she would possibly pay simply half of current administration charges. The charges she doesn’t pay are hers to maintain. The financial savings when compounded for years can translate into massive boosts to returns.

Lastly, Julia might use rising money move to pump up her parched TFSA with a gift stability of $4,000.

“Julia can resolve her debt issues. Then debt-free, elevate her disposable earnings in retirement,” Einarson explains. “The complexity of the method can be rewarded with a reliable retirement earnings.”

Retirement stars: Three retirement stars *** out of 5

Monetary Submit

electronic mail [email protected] for a free Household Finance evaluation

{kind=link}