This text is an on-site model of our Unhedged publication. Enroll here to get the publication despatched straight to your inbox each weekday

Good morning. It’s Katie Martin. Thrilling instances: Rob is on sabbatical this month. It is without doubt one of the finest perks of working on the FT, higher even than the well-known weekly cake trolley (accessible within the London workplace solely).

Whereas he’s away, I’m one of many folks invited to assist out. I’m tempted to make use of this chance to fangirl over the glorious Lionesses or trash a few of Rob’s most dearly held beliefs on his personal lovingly curated platform, for instance by extolling the virtues of Birkenstocks. He hates them, and he’s unsuitable. It is a hill I’ll die on.

I’ll see you once more subsequent week. Within the meantime, say hello at [email protected], or complain about stuff to [email protected].

Markets’ blended tales

Nobody is aware of what on earth is occurring. Or on the very least, market members are demonstrating terribly excessive ranges of intelligence by holding two opposed concepts of their thoughts on the similar time. Let’s say it’s the latter.

This commentary, from Adam Cole, a currencies analyst at RBC, is wonderful and sums up the purpose relatively effectively. The chart tells you that, sure, buyers assume the Fed will carry on jacking up rates of interest from right here (see the blue line), but additionally that very quickly after it’s executed, it should begin hacking them again once more (the black one):

That is bizarre, “solely unprecedented”, in reality, in Cole’s phrases. He provides:

Markets have by no means discounted vital Fed easing inside two years whereas the Fed was nonetheless in the course of a mountain climbing cycle.

So, you aren’t imagining it. We actually are swimming by means of highly effective cross currents in the meanwhile. The dominant theme is flipping from doom/despondency to cautious optimism at fairly a clip, which is sensible given this obvious confidence that the Fed will hike until it hurts.

For now, cautious optimism is successful. International developed market shares jumped by shut to eight per cent in July, partly resulting from some resilient earnings from tech megastocks that also have a (dangerously?) outsized affect on broad market path.

To make this make sense, once more, a number of conflicting issues must be true on the similar time. Recessions (correct ones) must be fine, actually, due to all the better financial coverage they suggest, and/or peak worry is over, and/or markets have already priced in sticky inflation and a tough touchdown.

Perhaps, like UBS Wealth Administration, folks have been crunching the numbers and figured that wait-and-see is for wimps. From UBS Wealth chief investor Mark Haefele’s be aware on Friday (my highlights):

Immediately, after a 26 per cent derating over the previous 12 months, the S&P 500 trades at a trailing price-to-earnings (P/E) ratio of 18.3x, a degree that since 1960 has been according to annualised returns in a wholesome 7-9 per cent vary over the following decade . . .

The concept ready might be riskier than investing instantly can also be borne out within the historic information. Since 1960, a method that waited for a ten per cent correction earlier than shopping for the S&P 500 after which bought at a brand new all-time excessive would have underperformed a buy-and-hold technique by 80x (sure, eighty). Over the identical time interval, a method of investing instantly after a 20 per cent drop would have delivered a median one-year return of 15.6 per cent. Staying in money for a yr after a 20 per cent drop comes at a big alternative value.

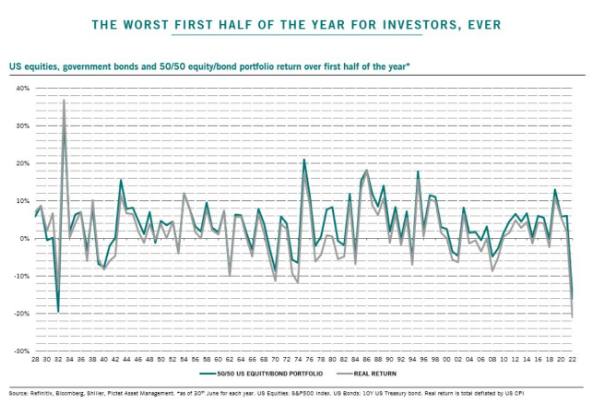

Positive, however there’s an actual hazard of overthinking all this. As Luca Paolini at Pictet Asset Administration factors out:

Preserve it easy. Equities and bonds are bouncing again primarily as a result of 1H2022 was the worst ever in actual return phrases. Worse than 1932!

His chart right here of how a theoretical 50/50 portfolio of US equities and authorities bonds would have carried out over near a century relatively hammers dwelling that time:

Regardless of the trigger, this rally might in a short time eat its personal tail. Brighter markets imply simpler monetary situations — the other of what the Fed desires to see, particularly after consecutive 75 foundation level fee will increase. This all simply provides the Fed a move to hit the brakes even more durable.

Readers with short-term funding horizons should be tempted to see how lengthy this has to run, and good luck to you. Traders with longer recreation plans are usually much less inclined to attempt to be a hero. A couple of days earlier than the most recent Fed’s supposedly dovish pivot, I requested Sonja Laud, chief funding officer at LGIM, whether or not inventory markets had capitulated but, whether or not it was time to be courageous and soar in.

“To me there’s no rush,” she stated. “Plenty of the large goalposts are shifting. We by no means actually appreciated the worth of the globalisation [that we saw] after the autumn of the Berlin Wall and the dissolving of the Soviet Union . . . Simply-in-time provide chains had been an enormous profit to shoppers globally and to the profitability of companies worldwide.”

Now, globalisation shouldn’t be precisely useless, however it’s fraying, reshaping profitability and inflation dynamics. “We’re saying goodbye to the American-led post-World Warfare Two order that all of us took as a right,” she stated. “It’s historical past within the making.”

Seen by means of that lens, it does appear untimely to declare this tough patch in markets to be over. The method of determining how provide chains and inflation cope within the face of scratchy geopolitics is not going to be fast, and false dawns will catch buyers out. All of the clichés are true: keep humble, keep nimble.

Catching Katie’s eye

The rising wager is that the Financial institution of England will increase charges by 50bp this week, as BoE governor Andrew Bailey has previously hinted. Doing 25bp is so pre-coronavirus pandemic.

Everybody hates Europe. “Traders take a recent optimistic have a look at Europe” is a staple of monetary journalism. I do know as a result of I’ve written or edited these tales myself on a number of events. Proper now, although, Europe is basically struggling to keep up a fan membership. Goldman Sachs stated on Friday it thinks the Euro Stoxx 600 has one other 10 per cent to fall this yr. “We predict the general market is just too complacent in regards to the weak point in progress and dangers associated to Russian fuel provide and Italian politics, that are skewed to the draw back,” wrote Sharon Bell and colleagues on the financial institution.

In contrast to each different massive equities index, the FTSE 100 is now optimistic on the yr. The primary individual to inform me that is the Truss Impact will obtain the toughest of stares.

For those who haven’t already, read this, on the Russian economic system. It’s not fairly. High line, once more with my spotlight:

a typical narrative has emerged that the unity of the world in standing as much as Russia has someway devolved right into a “struggle of financial attrition which is taking its toll on the west”, given the supposed “resilience” and even “prosperity” of the Russian economic system. That is merely unfaithful.

For those who can bear it, behold the myriad methods during which the crypto industrial complicated relieves folks of their cash and “Meet the ‘psychic’ cryptovoyants selling bitcoin info to thousands”. (Sifted, with a heroic definition of ‘data’ there.)

One good learn

We are able to’t get sufficient of Neom, Saudi Arabia’s part-fun, part-insane desert megacity. Its design jumps between “dystopian Dying Star evil empire, the apartheid structure of a post-apocalyptic security-city and a rendering of a glamorised and unlikely central enterprise district in search of gullible buyers”, writes the FT’s structure critic.

{kind=link}