The mortgage trade is extremely aggressive, with a whole bunch of lenders seeking to get your small business. However in relation to VA loans, you don’t need to go together with simply any lender. Most lenders don’t do many VA loans, and a few do none in any respect. Since VA loans are a extremely specialised mortgage sort, it’s finest to go together with lenders who focus largely and even totally on this mortgage sort.

That will help you with the choice, we’ve ready this information itemizing what we imagine to be the very best VA house loans of 2022. We’ll cowl every lender, then give you an intensive understanding of VA house loans and the way they work.

Earlier than we go any deeper, you’ll be able to scan the comparability desk beneath to get a fast overview of the eight finest VA mortgage lenders of 2022:

Our Picks for the Greatest VA Mortgage Lenders

We’re not going to maintain you ready – beneath is our listing of what we imagine to be the very best VA house loans of 2022, and what we imagine every is finest for:

Greatest VA Mortgage Lenders – Firm Opinions

Beneath are abstract critiques of every of the eight finest VA house loans for 2022. Below every abstract assessment is a hyperlink to our full assessment of every explicit lender. Be at liberty to click on by way of should you’d like extra data earlier than making a call on which VA lender to make use of.

Veterans United takes our high honors as the very best total VA mortgage lender. It’s simple to see why. It’s the most important VA mortgage lender within the nation and one which specializes totally in working with veterans.

For instance, the corporate works with senior members of all branches of the US army, together with the Military, Navy, Air Power, and Marine Corps, to assist them keep on high of developments affecting veterans. Additionally they supply their Veterans United Lighthouse program. Not solely does it assist veterans to construct and enhance their credit score, however it additionally supplies a community of actual property brokers nationwide who’re educated in VA house purchases.

Why We Like Veterans United: Having the standing of the most important VA mortgage lender within the nation means veterans are trusting their house financing must Veterans United greater than some other lender. We additionally like that the corporate focuses totally on VA loans, so that they aren’t distracted by different mortgage applications.

Professionals

- Supplies solely VA mortgages, enabling the corporate to specialize on this distinctive mortgage sort.

- Presents specialised VA mortgage applications, just like the VA Power Environment friendly Mortgage.

- The corporate has a powerful status, together with an A+ ranking from the Higher Enterprise Bureau.

Cons

- The corporate has bodily branches in solely 17 states, so not everybody can have a possibility to get pleasure from face-to-face contact.

- Since Veterans United solely handles VA loans, they might not be capable to assist in case your wants will likely be higher served by a traditional mortgage.

See Our Full Veterans United Review

USAA tends to be on the low finish of the rate of interest spectrum with VA loans. However there’s much more to USAA than simply VA loans. It’s a full-service monetary supplier providing a wealth of monetary providers designed particularly for veterans. Along with banking, insurance coverage, and investments, the corporate focuses on auto insurance coverage, the place it constantly ranks on the high of the listing for the complete trade.

USAA supplies the complete vary of VA loans, together with fastened and adjustable-rate mortgages, in addition to jumbo loans. In the meantime, their USAA Dwelling Studying Heart will assist to coach veterans on the various particulars of the mortgage lending course of.

Why We Like USAA: Not solely does USAA present low charges, however in addition they supply all kinds of monetary providers for veterans. That features banking, insurance coverage, and investments.

Professionals

- Persistently low mortgage charges.

- Presents a full vary of monetary providers, particularly automotive insurance coverage applications that will very properly be the very best within the nation.

- Additionally presents typical loans, that are generally extra helpful for veterans than a VA mortgage will likely be.

- USAA has a powerful status, together with an A+ ranking from the Higher Enterprise Bureau.

Cons

- Doesn’t supply FHA loans.

Although it’s not broadly recognized, Quicken Loans is the most important retail mortgage lender in the complete nation. However mortgage financing is obtainable by way of their on-line lending portal, Rocket Mortgage. It supplies a full vary of mortgage merchandise, together with typical and FHA loans, along with VA loans. That’s vital as a result of if a VA mortgage is just not the best choice, Quicken Loans can current options.

Quicken Loans will get our vote as the very best on-line VA mortgage lender. That’s as a result of the complete lending course of takes place on-line, so you’ll be able to apply and monitor your progress from the consolation of your private home or place of employment. You can even add a lot of the required documentation wanted for the mortgage software course of, proper on the web site.

Why We Like Quicken Loans: The corporate web site signifies Quicken Loans will settle for a debt-to-income ratio (DTI) as excessive as 60%. That is properly above the conventional most of 43%.

Professionals

- Most likely the very best on-line mortgage expertise within the trade.

- Not solely are you able to add requirement documentation on the web site, however the firm additionally performs a lot of the verification course of instantly with employers and monetary establishments.

- Accommodate very excessive debt ratios for VA loans.

- Quicken Loans has a powerful status, together with an A+ ranking from the Higher Enterprise Bureau.

Cons

- No face-to-face contact – Quicken Loans has no bodily branches and operates totally on-line.

See Our Full Quicken Loans Review

With PenFed Credit score Union, quick for Pentagon Federal Credit Union, it needs to be apparent this lender has a powerful orientation towards VA loans. In reality, it primarily supplies providers for these employed by the US authorities and its companies. Along with mortgages, in addition they present auto loans and bank cards. PenFed additionally presents FHA loans, in case that may be a more sensible choice than a VA mortgage.

Why We Like PenFed Credit score Union: PenFed costs no lender charges, like origination or software charges. The one closing prices you’ll pay will likely be these charged by third events, like attorneys, appraisers, and title corporations. The credit score union additionally supplies as much as $2,500 in lender credit, which can be utilized towards third-party closing prices and different bills.

Professionals

- Prices no lender charges, decreasing your closing prices considerably.

- Additionally presents a $2,500 lender credit score to cowl different closing prices.

- Presents FHA loans, along with VA loans.

- Like a lot of the different lenders on this listing, PenFed has a wonderful status, together with an A+ ranking with the Higher Enterprise Bureau.

Cons

- Doesn’t supply typical mortgages.

- As is the case with most credit score unions, you have to to open a deposit account to qualify for a mortgage.

See Our Full PenFed Credit Union Review

Navy Federal Credit Union is the most important credit score union in the US, and by a really vast margin. And though the title contains “Navy,” they welcome members of all different branches of the US Armed Forces. On the credit score union, you’ll be able to benefit from banking providers, like deposit accounts, auto loans, and bank cards, along with house mortgages.

Navy Federal additionally supplies typical and FHA loans, along with VA loans.

Why We Like Navy Federal Credit score Union: The truth that this lender is a credit score union, and one which caters to army households, makes it a best choice for first-time homebuyers.

Professionals

- Full-service credit score union, offering deposit accounts, auto loans, and bank cards.

- Caters to members of the US army.

- Presents typical and FHA loans, offering broader house financing choices to veterans.

Cons

- As a credit score union, you may be required to grow to be a member by opening and sustaining a deposit account with the establishment.

- Not rated by the Higher Enterprise Bureau, which is not essentially a destructive. But it surely does imply there’s restricted data on customer support outcomes.

See Our Full Navy Federal Credit Union Review

LendingTree is an internet mortgage market, the place dozens of lenders supply their mortgage applications to shoppers. Not solely does it embrace mortgages, however you too can discover automotive loans, bank cards, private loans, and different monetary merchandise on the platform. LendingTree is just not a direct lender, however the web site is free to make use of.

In fact, the benefit of procuring on an internet market is that you may additionally contemplate different financing choices. Along with VA loans, taking part lenders additionally supply typical and FHA loans.

Why We Like LendingTree: It’s a wonderful selection for anybody who’s primarily searching for the bottom mortgage price. By finishing a easy on-line mortgage software, you’ll get presents from a number of lenders. You possibly can then select the lender that gives the very best mixture of charges and phrases.

Professionals

- Free, easy-to-use web site.

- Allows you to get mortgage presents from a number of lenders so you’ll be able to select the very best deal for you.

- A superb selection should you’re searching for different mortgage sorts, like automotive loans, bank cards, and private loans.

Cons

- Whereas you will get mortgage presents from a number of lenders, you have to to finish a full software on the lender’s web site when you make your selection.

- Selecting a mortgage lender primarily based totally on low charges opens the potential to decide on a lower than respected lender.

See Our Full LendingTree Review

Wells Fargo is just not solely one of many largest mortgage lenders within the nation but in addition one of many very greatest industrial banks. Meaning you’ll be able to get pleasure from full-service banking, together with checking, financial savings, CDs, entry to all kinds of mortgage applications, and even small enterprise banking – with the identical firm you get your mortgage from.

Wells Fargo supplies all forms of mortgage financing, together with typical and FHA loans, in addition to VA mortgages. And as a financial institution, in addition they supply secondary financing, together with house fairness loans and residential fairness traces of credit score (HELOCs). Eligible VA debtors must also bear in mind that Wells Fargo doesn’t cost an origination charge on VA loans.

Why We Like Wells Fargo: Full-service financial institution that may accommodate all of your monetary wants, together with small enterprise banking in case you are self-employed.

Professionals

- Full-service financial institution, offering all banking providers, together with small enterprise banking for the self-employed.

- Accessible in all 50 states.

- Presents typical and FHA loans, in addition to secondary financing.

- No origination charge is charged on VA loans.

- That is one other lender with a wonderful status, together with an A+ ranking from the Higher Enterprise Bureau.

Cons

- Since Wells Fargo presents so many alternative merchandise and mortgages, they do not essentially concentrate on VA loans.

See Our Full Wells Fargo Review

loanDepot is a direct lender that, very similar to Quicken Loans, operates totally on-line. That may make for a simple and handy mortgage course of, together with the power to add required supporting documentation, proper on the web site.

loanDept is a direct lender, so that you might be assured you may be working with them by way of the complete mortgage course of. The corporate operates in all 50 states, in addition to Washington, DC. Although it’s not as well-known as a number of the different lenders on this listing, it’s truly the fifth largest mortgage lender within the nation.

Why We Like loanDepot: They provide the complete vary of mortgage financing merchandise, together with typical and FHA loans, in addition to secondary financing choices, along with VA mortgages.

Professionals

- The net mortgage course of is fast and handy and might be achieved from the consolation of your private home or workplace.

- Presents all different mortgage financing choices that will higher serve your wants than a VA mortgage.

Cons

- The all-online side of the corporate eliminates face-to-face contact, should you occur to favor the non-public contact.

- Like Wells Fargo, loanDepot is a diversified lender, it doesn’t concentrate on VA mortgages.

- Not rated by the Higher Enterprise Bureau, so you may want to hunt out different ranking providers to find out their customer support status.

Get a free quote from the #1 VA Lender within the nation!

VA Dwelling Loans applications supply that will help you purchase, construct, or enhance a house in addition to refinance your present house mortgage. Click on beneath to get began!

VA Dwelling Mortgage Information

How does a VA mortgage work?

In most respects, VA loans work like some other sort of mortgage, together with typical and FHA loans. The primary distinction is that you simply have to be an eligible veteran or an active-duty member of the US army to qualify for a VA mortgage.

You must also bear in mind that VA loans are solely out there for owner-occupied, main residences. If you wish to buy a trip house or rental property, you’ll want to contemplate a traditional mortgage as a substitute.

Most likely the most important benefit of VA loans is that they supply 100% financing. Not solely will that eradicate the necessity for a down cost, but in addition for a second mortgage or a house fairness line of credit score (HELOC). Although HELOCs have grow to be frequent for householders, it’s at all times finest to know the pros and cons of a HELOC. Although they’ve particular benefits, there are specific dangers. Both manner, they’re often not obligatory should you qualify for a VA mortgage.

VA loans can be found for each purchases and refinances. Charges and charges are decrease once you do an Curiosity Charge Discount Refinance Mortgage (IRRRL), versus a cash-out refinance. It’s vital to know when to refinance, then to work with the best mortgage refinance companies for VA loans.

Due to the 100% financing issue, refinances might be extra difficult with VA loans than with typical loans.

Whether or not you might be buying or refinancing, it’s vital to know how to get the best VA loan rates. Below “The best way to qualify for a VA mortgage” beneath, we’ll go over the components that may have an effect on the speed you’ll pay.

What’s the VA funding charge?

Whenever you make a down cost of lower than 20% utilizing a traditional mortgage, you’ll be required to pay what’s often known as non-public mortgage insurance coverage, or PMI. That is an insurance coverage coverage you because the house owner are required to buy to partially compensate the mortgage lender do you have to default on the mortgage.

VA mortgages don’t use PMI. As a substitute, they’ve what’s known as the VA funding charge. It is a charge collected by the Veterans Administration, which is able to partially compensate lenders for borrower default on the mortgage. That is particularly vital with VA loans since they contain 100% financing.

The VA funding charge is paid on the time of closing. If it isn’t paid by the property vendor, lender, or by a present from a member of the family of the borrower, it will likely be added to the mortgage quantity. That is the commonest situation.

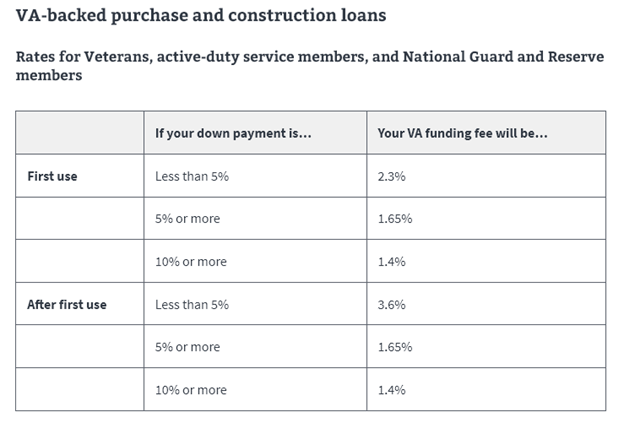

For instance, on most purchases, the funding charge will likely be 2.3%. If the mortgage quantity is $300,000, the quantity owed will likely be $306,900 with the VA funding charge added to the principal quantity of the mortgage. The borrower will then successfully pay the funding charge over the lifetime of the mortgage.

There are numerous charges that apply to the VA funding charge. These rates are as follows for 2022:

The VA funding charge is totally different for refinances. In case you are doing an Curiosity Charge Discount Refinancing Mortgage (IRRRL), during which you might be refinancing solely to decrease the rate of interest and cost in your mortgage, the charge is 0.5%.

In case you are doing a refinance and taking money out with the mortgage, the VA funding charge will likely be 3.6%.

Only for comparability’s sake, typical mortgages cost month-to-month mortgage insurance coverage premiums, which VA loans don’t have. FHA loans have each upfront and month-to-month premiums.

When you do have so as to add the VA funding charge to your mortgage quantity, consider it as one of many costs of owning a home. With regards to VA loans, the funding charge is an enormous cause why you’ll qualify for the mortgage.

Professionals and Cons of a VA mortgage

Professionals

- VA loans don’t require the borrower to make a down cost.

- Closing prices are sometimes paid by the vendor or the lender.

- No month-to-month mortgage insurance coverage premiums are required.

- VA loans might be simpler to qualify for than FHA and traditional loans.

- Straightforward to refinance in case you are doing a no-cash-out mortgage from one VA mortgage to a different.

Cons

- Accessible just for eligible veterans and active-duty members of the US army.

- Can’t be used for the acquisition of a trip house or funding property.

- The VA funding charge is added to the mortgage quantity, barely rising the month-to-month cost.

- Some sellers favor to not entertain presents involving VA loans, on account of potential property repairs and paying borrower closing prices.

What’s the VA mortgage restrict?

For 2022, the standard maximum VA loan amount is $647,200 for a single-family property. Nevertheless, in areas designated as “excessive value,” the utmost mortgage quantity might be as excessive as $970,800. The utmost limits are larger for owner-occupied houses with 2-to-4 dwelling models in them.

However even if you wish to buy a house for greater than the usual most, you are able to do so utilizing the VA Jumbo program. That’s a program that allows you to purchase a higher-priced house, however that may require you to make a partial down cost.

It really works like this: let’s say you need to buy a house for $847,200. That’s $200,000 above the usual most mortgage restrict.

When you solely wanted to borrow the utmost of $647,200, you may accomplish that with no down cost by any means. However beneath the VA Jumbo mortgage program, you’ll be required to make a down cost equal to 25% of the quantity by which the mortgage exceeds the usual most.

Because the property you might be buying is priced $200,000 over the usual most restrict, you’ll must make a down cost equal to $50,000, which is 25% of $200,000.

Which will seem to be an enormous chunk of cash. However $50,000 represents a down cost of slightly below 6% on a house value $847,200.

That’s an impressive deal since typical Jumbo loans sometimes require a 20% down cost.

The best way to qualify for a VA mortgage?

To be eligible for a VA mortgage, you have to be both an active-duty member of the US army or an eligible veteran. Eligibility is set by buying a VA Certificate of Eligibility (COE). You might have acquired this certificates upon discharge from the army, however don’t fear should you didn’t. Your mortgage lender will help you in acquiring the certificates.

Whether or not you’re a veteran or at the moment on lively obligation, there are specific requirements for that eligibility primarily based on once you served and the way lengthy. Eligibility won’t be granted should you had been dishonorably discharged.

Aside from VA eligibility, you’ll be able to qualify for a VA mortgage the identical manner you’ll with some other mortgage program. Whereas the next data will aid you to know the method, it’s finest to let a lender present you how to get approved for a home loan.

Different Issues Your Lender Will Look At

Credit score. The Veterans Administration doesn’t set a selected minimal credit score rating, however relatively leaves it as much as particular person lenders. Most lenders set the minimal rating at 620, although some will go decrease. The lender can even contemplate particular person parts of your credit score, comparable to any historical past of chapter, foreclosures, or critical delinquencies.

Simply as is the case with different forms of mortgages, your credit score can have a powerful influence on the speed you’ll pay in your mortgage. You should definitely test current mortgage rates primarily based in your present credit score rating.

Employment. Lenders will typically search for a steady historical past of employment of no less than two years. Navy service or faculty can partially or totally fulfill this requirement, so long as you’ve gotten the promise of employment in a job associated to your army or faculty expertise.

Debt ratio. VA typically prefers your whole fastened obligations, together with each the brand new housing cost and any recurring debt funds, to be inside 43% of your secure month-to-month revenue. Nevertheless, lenders will generally go larger when you have compensating components, like a down cost, money reserves after closing, or wonderful credit score.

Your debt ratio will likely be a significant factor in answering the query, how much house can I afford?

Down cost. Since VA loans are well-known for offering 100% financing, a down cost is often not required.

Closing prices. These might be paid by the borrower, but in addition by the vendor, the lender, or by a present from a member of the family.

Varieties of VA loans out there

VA loans can be found in three fundamental sorts, fixed-rate, adjustable-rate (ARM), and Jumbo loans.

Mounted-rate

These are mortgages with phrases starting from 15 years to 30 years and carry a hard and fast price and month-to-month cost. Although the rate of interest on a hard and fast price is larger than it will likely be for an ARM, it’s a a lot much less dangerous mortgage because the cost won’t ever change. This will likely be significantly vital if rates of interest rise sooner or later.

Earlier than selecting a 15-year mortgage, which has the next month-to-month cost, it’s best to first contemplate the implications of a 15 vs. 30-year mortgage. For many debtors, the 30-year mortgage will supply a decrease cost, which will likely be a extra comfy match.

ARM

This mortgage sort has a fixed-rate time period, which is adopted by annual changes. For instance, with a 5/1 ARM, you’ll have a hard and fast price for the primary 5 years of the mortgage. After that, the speed will change annually. To maintain the funds from going too excessive upon adjustment, ARMs have price caps.

For instance, in a typical association, the speed will be unable to extend greater than 2% on the primary adjustment. Subsequent changes will equally be restricted to 2%, with a most adjustment of 5% over the lifetime of the mortgage.

Nevertheless, even with the speed caps, your price and cost can go up considerably from the preliminary time period. If the mortgage begins at 4% and has a 5% lifetime cap, it’s possible you’ll ultimately find yourself paying 9%. These loans are appropriate provided that you intend to remain within the house for not more than the preliminary fixed-rate time period of this system.

Jumbo loans

We lined this earlier beneath “What’s the VA mortgage restrict,” so we gained’t go into any element right here. A VA Jumbo mortgage is solely a program that permits an eligible borrower to borrow greater than the usual mortgage quantity, in change for making a down cost equal to 25% of the surplus mortgage quantity. Earlier than taking a jumbo mortgage, remember to achieve an intensive understanding of the VA Jumbo loan. The upper greenback quantity does signify a better threat.

VA loans have many potential advantages for debtors, together with as much as 100% financing, no mortgage insurance coverage, no down cost, no prepayment penalties, and aggressive rates of interest. Nevertheless, these loans are solely out there to present and former service personnel and their surviving spouses.

How does one qualify for a VA mortgage?

To qualify for a VA mortgage and get a Certificates of Eligibility (COE), debtors should meet the service standards set by the VA (which think about the size of service, its character, and obligation standing) — in addition to your lender’s credit score and revenue necessities. Spouses should additionally acquire a COE, and their servicemember partner should meet sure descriptions laid out by the VA.

What are the closing prices for a VA mortgage?

VA mortgage closing prices fluctuate relying on a number of various factors, together with the placement of the house, the lender, and the house sort itself. You might have to pay a VA funding charge, mortgage origination charge, VA appraisal charge, inspection charges, hazard insurance coverage, title insurance coverage, householders affiliation charges, and a recording charge — in addition to actual property, state, and native taxes. Do you have to select to purchase factors to decrease your rate of interest, these would additionally must be paid. To provide a common concept, VA closing prices typically common between 3 and 5 p.c of the overall mortgage quantity.

What’s the VA mortgage restrict?

VA house mortgage limits are the identical as these for the Federal Housing Finance Company’s conforming mortgage limits. For 2022, that is $647,200 as a nationwide baseline, which grows to $970,800 in high-cost areas.

How We Discovered the Greatest VA Mortgage Lenders

There are various mortgage lenders providing VA loans, however solely a small share specialize on this mortgage sort. To give you our listing of the eight finest VA loans for 2022 we thought of the next standards:

The variety of VA loans the lender does.

- Specialization in VA loans.

- The variety of VA mortgage applications the lender presents.

- The lender’s status.

- Specializations, like accommodating low credit score scores, low closing prices, and different providers provided by the lender.

As well as, we selected lenders that cowl vast geographic areas to profit as many individuals as potential.

Abstract of the Greatest VA Dwelling Loans of 2022

We imagine any one in every of these lenders will likely be a wonderful option to give you a VA mortgage.

{kind=link}