Do you know the common financial institution is paying .06% in curiosity on their financial savings accounts? That appears loopy sufficient by itself, however it’s even crazier that my financial institution is paying even lower than that.

That’s proper; my very own financial institution is paying a fraction of the common financial savings rate of interest….really .01%. Even worse, my financial institution (U.S. Financial institution) has been paying near the identical paltry price for years.

I feel my financial institution hates me. Are you able to relate?

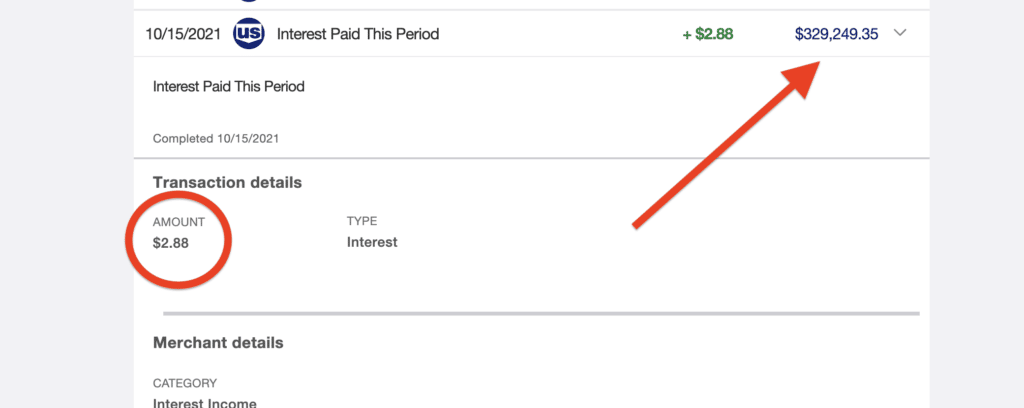

You’ll be able to see precisely what I imply within the screenshot under. I’ve greater than $329,000 in considered one of our financial savings accounts, and I solely earned $2.88 in curiosity through the month I grabbed this photograph.

That’s fairly unhappy when you consider it, however I do know I’m not alone. Half the folks studying this put up are most likely incomes about that a lot on their financial savings if something in any respect.

Everyone knows that rates of interest have been hovering at or close to document lows for years, and banks can provide nearly nothing consequently.

Fortuitously, we don’t must accept incomes next-to-nothing on our financial savings accounts. Actually, there are a number of banking alternate options to earn extra in your financial savings than what a conventional financial institution will provide.

One of many choices I share on this put up is paying 850X greater than the common conventional financial institution!

Earlier than we dive into the highest banking alternate options although, I do wish to say how essential it’s to have an emergency fund. It’s at all times potential you’ll lose your job or face an unpredictable monetary emergency, and your long-term financial savings could possibly be the one factor that helps you keep away from every kind of monetary mayhem (you’ll be able to take a look at a few of the best savings account rates right here).

Some consultants say it is best to have three to 6 months of bills stashed away in emergency financial savings, and I are inclined to agree. Nonetheless, I feel you have to tailor the dimensions of your emergency fund to your distinctive state of affairs and wishes.

For instance, it’s possible you’ll wish to have a much bigger emergency fund if you happen to’re self-employed or you may have youngsters, whereas you will get away with a smaller e-fund if you happen to’re single, you may have actually low bills, or your job is extraordinarily safe.

Both means, the banking alternate options I’ll dive into under are not to your core emergency financial savings. In any case, you need your e-fund in a safe account with FDIC insurance coverage. It’s possible you’ll not earn plenty of curiosity with an everyday financial institution, however you received’t lose any cash out of your financial savings, both.

Additionally, observe that you may take a look at my banking alternate options podcast on Spotify if you happen to favor listening over studying. You’ll be able to take a look at the podcast episodes here and here.

9 Banking Options to Earn Extra Curiosity

With that in thoughts, the banking alternate options I like to recommend are for any extra funds you may have along with your true emergency financial savings. That is cash you received’t essentially want within the subsequent few years, so you’ll be able to tackle extra danger.

Which banking alternate options am I speaking about? I break down all 9 of them under.

#1: Neobank

“Neobank” is considerably of a hipster time period used to explain an online-only financial institution that doesn’t have any brick and mortar areas. This doesn’t imply Neobanks aren’t actual; it simply means you received’t drive round and run right into a bodily financial institution location. And with out a bodily location to take care of, these banks have decrease overhead. This implies they will pay you extra curiosity in your financial savings.

I not too long ago learn that there have been greater than 300 digital banks world wide. A number of the greatest embody SoFi, which began off extra as a scholar mortgage refinancing firm. One other on-line financial institution value noting is Chime Financial institution, which is presently paying an 0.50% annual share yield (APY) on its financial savings accounts.

Lending Club is yet one more on-line financial institution that has been round for some time. Lending Membership was a peer-to-peer lender, however they now provide a web based financial savings account that’s presently paying a 0.60% annual share yield.

#2: Treasury Inflation Protected Securities (TIPS)

Should you assume inflation is simply going up from right here, Treasury Inflation-Protected Securities (TIPS) may present a wonderful place to stash your extra money. TIPS mechanically adjusts primarily based on the CPI Index, which is the Shopper Value Index that measures the costs of various items and providers. This makes it one other nice banking various.

Whereas some might disagree that TIPS is definitely maintaining with inflation, you’ll be able to go to TreasuryDirect.gov to learn extra about this funding possibility and different bonds which are issued by the federal government.

TIPS are issued in increments of $100, so you must have at the least $100 to get began investing. One other main good thing about TIPS is the actual fact you don’t must pay state or native taxes in your returns. Word: With TIPS, you do must pay federal taxes in your positive aspects.

#3: On-line Funding Apps

On-line funding apps (a.okay.a. on-line brokerage providers) are one other nice banking various that embody firms like Robinhood and M1 Finance. When most individuals consider these firms, they could mechanically consider meme shares or crypto investing. Nonetheless, these apps even have a money administration account that pays a good price of return.

With Robinhood, for instance, the money administration part of the app has a financial savings part that pays .30% APY. Not solely that, however this account from Robinhood comes with no hidden charges. You’ll be able to even use your account to get money at greater than 75,000 fee-free ATMs nationwide. Higher but, Robinhood consists of FDIC Insurance coverage on its money administration accounts.

M1 Finance additionally boasts its personal finance “tremendous app” that can really set you again $125 per yr. Nonetheless, this account pays a 1% rate of interest, and also you get a debit card that pays 1% cashback every time you employ it.

Whereas paying $125 per yr for a web based account and debit card can appear actually excessive, take into account that you’ll earn 33X the nationwide common financial savings price in your deposits. Because you get 1% again on debit card purchases, you may have the potential to make up for that payment in a rush and nonetheless find yourself forward.

Make investments as little or as a lot as you need with a Robinhood portfolio.

#4: Excessive-Yield Bonds

Most individuals consider bonds as being extraordinarily secure, and they’re. Nonetheless, folks buy bonds so much in another way than they did a number of a long time in the past.

The newborn boomer technology went out and bought particular person bonds straight from the issuer, whether or not they had been municipal bonds or one thing else. Nonetheless, a lot of immediately’s traders buy their bonds by mutual funds or ETFs.

One instance of a mutual fund with high-yield bonds is the American Century Excessive-Earnings Yield Fund (NPHIX). The present yield on this fund is 5.12%, though this fund has extra danger. This implies it’s doubtless your stability will go up and down over time.

One other instance is the Nuveen Excessive Yield Municipal Bond Fund (NHMRX), which comes with a yield of three.09%. As soon as once more, this can be a high-yield bond with larger danger, so you may have the potential to see your stability fluctuate over the long-term.

There are additionally fairly just a few ETFs with high-yield bonds together with the SPDR Excessive-Yield Bond ETF (JNK) with a yield of 4.75%. This kind of bond is taken into account a junk bond, so the JNK image on this one is definitely kinda humorous.

Should you’re questioning the place to purchase high-yield bonds, you received’t must look far. You’ll be able to spend money on high-yield bonds by all of the common on-line brokerage companies and apps, equivalent to M1 Finance, Robinhood, and E*TRADE. These may all be nice various banking alternate options for extra funds.

#5: Excessive-Yield Shares

In terms of high-yield shares, they’re structured so that they must pay out a good dividend, making them an ideal various to conventional banking. A number of the dividends on these shares provide you with a return that’s a lot larger than you’re incomes at your financial institution, though there may be extra danger concerned as properly.

For probably the most half, I’m speaking about shares which are listed throughout the Dividend Aristocrats. It is a record of 65 dividend shares which are listed within the S&P 500 with a historical past of accelerating their dividend during the last 25 years. This largely consists of extra established, blue-chip-type firms which have an extended historical past of making returns.

For instance, AT&T is part of this group with a dividend yield of seven.79%. One other one is McDonald’s, which presently has a dividend yield of two.11%. Verizon can also be included, with a dividend yield of 4.79%.

#6: Blended Portfolio

The sixth banking various I wish to speak about is having a blended portfolio that features a few of the choices above. For instance, you’ll be able to take a few of your extra financial savings and spend money on high-yield shares, then throw one other portion of your funds into high-yield bonds.

This technique is simple if you have already got an account with a platform like Robinhood or M1 Finance. As soon as your money administration account is open and also you get accustomed to utilizing these apps, you can begin branching off into different sorts of investments with ease.

Simply take note how some apps can work higher for making a blended portfolio. With Robinhood, for instance, you would need to select your individual funds and rebalance them over time. Nonetheless, M1 Finance presents funding “pies” which are expertly crafted to go well with several types of traders primarily based on how a lot danger they wish to take.

Betterment is one other on-line platform that makes it straightforward to tailor your funding portfolio to your timeline and targets. Nonetheless, this firm is a robo-advisor that makes use of expertise that will help you choose investments to your portfolio. For that cause, Betterment is healthier for individuals who need entry to funding administration providers they will’t get with an everyday investing app.

No matter platform you resolve to make use of, a blended strategy might help you earn the next price of return in your financial savings with out “betting the farm” on one particular technique.

#7: Actual Property Funding Trusts (REITs)

Whereas some particular person shares are labeled as REITs, that’s probably not what I’m speaking about right here. As an alternative, I’m speaking about choices that allow you to get publicity to actual property with the promise of a pleasant yield.

The primary possibility I wish to speak about is definitely an ETF. The iShares US Actual Property ETF (IYR) has returned 11.25% during the last ten years with a dividend yield of two.06%. That’s not half dangerous in any respect, particularly when you think about that you just by no means must set foot into the buildings you’re investing in.

And actually, that’s the key good thing about investing in actual property ETFs. You get publicity to the true property market with out having to hunt for properties or take care of the grunt work of being a landlord. You might be placing your cash in danger, however you may have the potential to attain a a lot larger return.

Another choice I like and use myself is named Fundrise. With this on-line actual property platform, you get to take a position straight into an REIT with out coping with the middlemen prices concerned in ETFs.

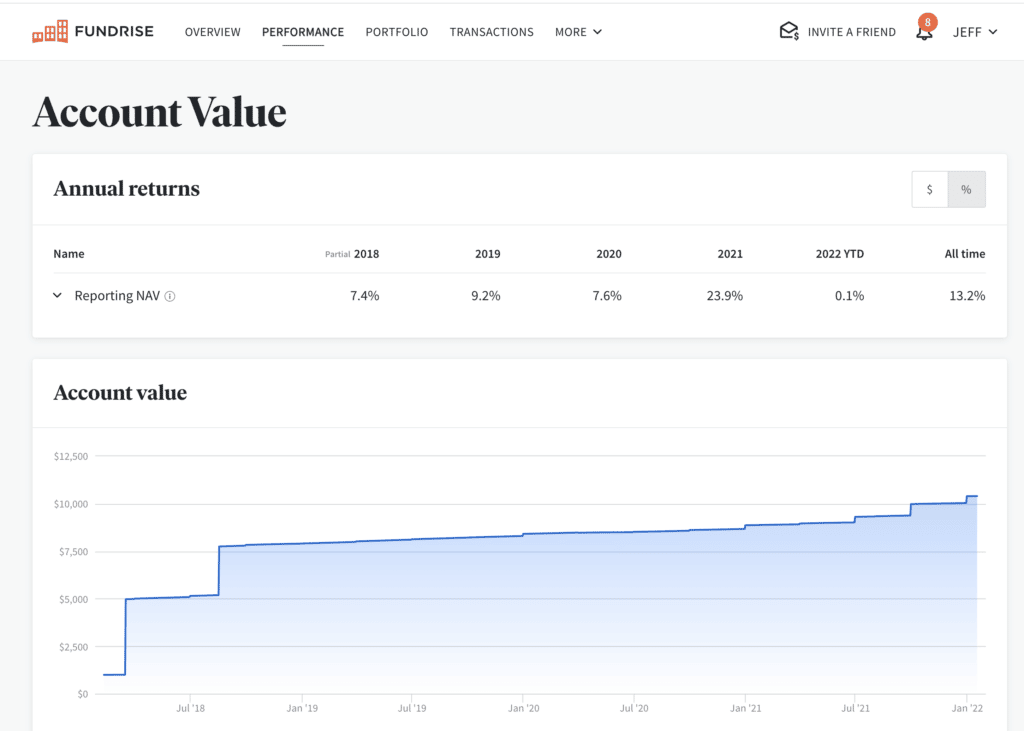

I began investing in Fundrise again in 2018, so I’ve had my account for a number of years by now. Loopy sufficient, my present all-time return is 13.2%, which you’ll see within the screenshot under.

One other cool factor about Fundrise is the actual fact you don’t must have an enormous amount of money to get began. The minimal funding with Fundrise begins at simply $10, and their primary starter degree is simply $1,000.

This implies you can begin investing in actual property with a fraction of the money you would wish to take a position into bodily property. Higher but, Fundrise makes it straightforward to get a deal with on the precise properties you’re investing in, whether or not that features a mall, an condo constructing, or some kind of business rental property.

Should you’re contemplating this selection, be certain that to learn my Fundrise review.

#8: Brief-Time period Word

To benefit from banking various #8, you have to be an accredited investor. This implies you have to make $200,000 per yr by yourself or $300,000 together with your partner, and also you want a internet value of greater than $1 million {dollars} not counting the worth of your major residence.

Should you meet these standards, carry on studying about Brief-Time period Notes and the way they work. If not, be at liberty to maneuver onto banking various #9!

Both means, short-term notes are provided by firms like YieldStreet. With a short-term observe from this on-line platform, you’ll be able to earn 40X the nationwide common cash market yield or an annualized yield of 4%.

These notes come freed from charges and bills, and so they’re a short-term product with liquidity provided in as little as six months. Brief-term notes from this firm additionally pay month-to-month curiosity funds on to your YieldStreet pockets.

Whereas these investments are focused at accredited traders with huge portfolios, the minimal funding quantity within the YieldStreet Brief Time period Word Collection XLIV is simply $500. Meaning you will get began with a comparatively small quantity, then see the way it goes from there.

#9: Crypto Financial savings Accounts

Lastly, let’s speak about the best way to make cash on crypto you may have with out really promoting it. Crypto savings accounts pay you a yield in your crypto deposits identical to you earn curiosity on an everyday financial savings account. I heard about this from one other investor a number of years in the past, and it nearly appeared too good to be true.

Throughout my first experiment with this banking various, I purchased $25,000 in steady coin investments and saved them in a BlockFi Curiosity Account. In the end, I used to be shocked to see my BlockFi account earned extra curiosity than my conventional financial savings account, which had greater than $300,000 in it.

In fact, you don’t must spend money on steady cash to earn curiosity. The BlockFi account additionally pays out curiosity on different sorts of crypto, equivalent to Bitcoin.

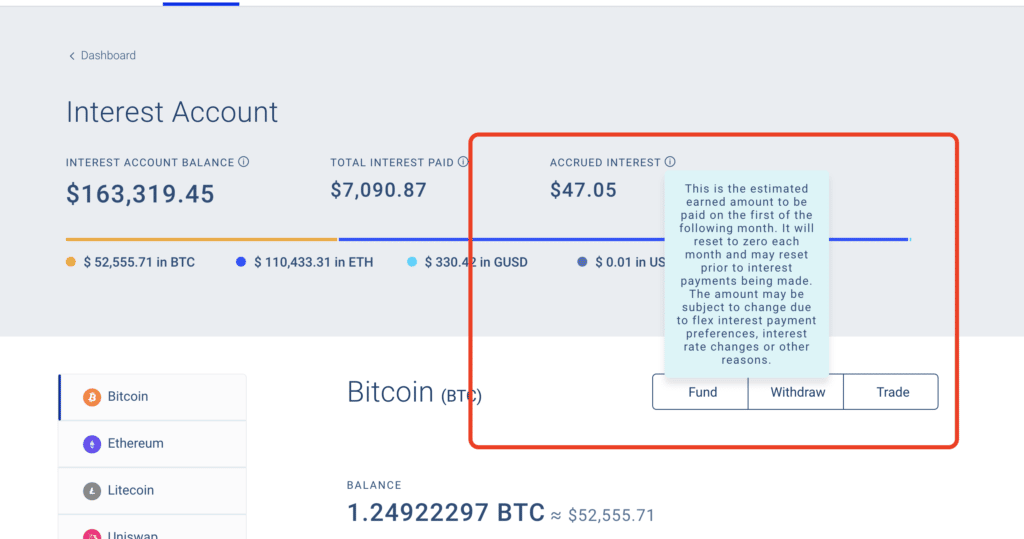

For the time being, I’ve round $165,000 in my BlockFi account, which is generally made up of Bitcoin and Ethereum belongings. On that quantity, my BlockFi account has paid greater than $7,000 in curiosity since I opened it.

See the screenshot under for proof:

While you examine that to the $2.88 per thirty days I’m incomes on my account with U.S. Financial institution, it’s straightforward to see what an enormous distinction this makes!

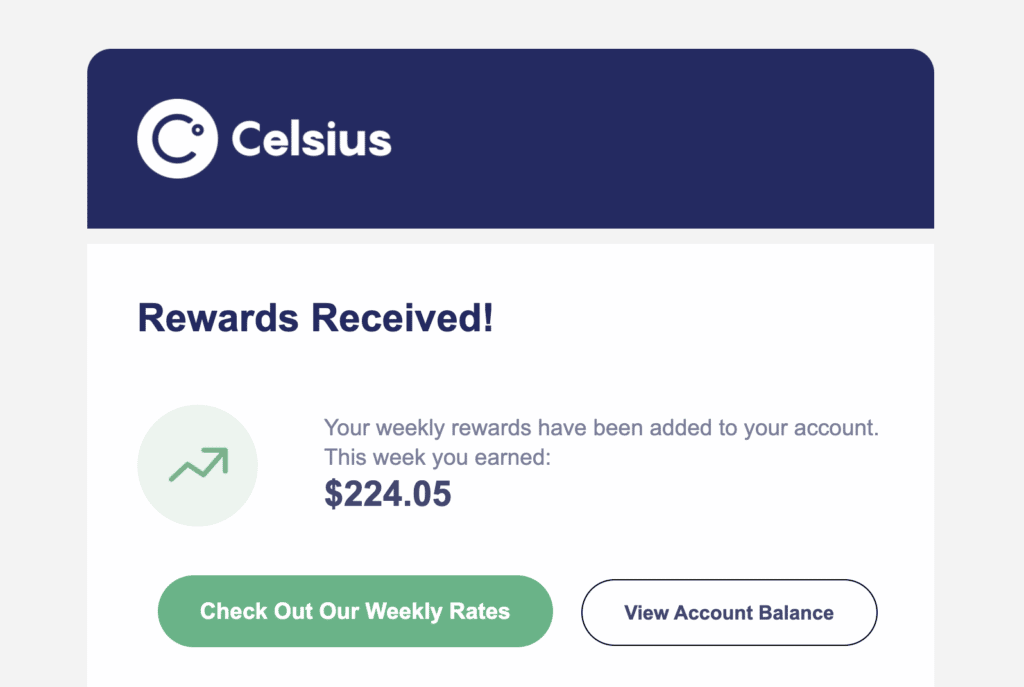

In fact, BlockFi isn’t the one firm with a crypto financial savings account. I even have an account with an organization known as Celsius, which I opened upon suggestion from a pal.

I presently have slightly below $200,000 in my account from Celsius, which is paying a yield of 8.5%. Curiously, Celsius pays out their curiosity weekly as a substitute of month-to-month like BlockFi.

As you’ll be able to see from the screenshot under, I’m presently incomes greater than $224 in curiosity from Celsius each week. That’s greater than $900 in curiosity each month, and properly over $11,000 in curiosity over the course of a yr!

That’s a lot greater than I’m incomes at U.S. Financial institution it really makes me wish to puke!

Simply take into account that investing in crypto and making money from crypto requires a ton of danger. There is no such thing as a FDIC insurance coverage, and there are not any ensures you received’t lose your whole funding.

The Backside Line

I hope this record of banking alternate options has you occupied with your cash and the best way to make it develop. In any case, it’s solely pure to wish to earn the next return in your financial savings, whether or not we’re speaking about your emergency fund or different money you may have stashed away for the long-term.

With that being stated, it’s essential to do not forget that larger yields at all times equal the next degree of danger. Options to conventional banks might give you extra curiosity in your deposits, however you’re giving up some safety alongside the way in which.

{kind=link}