You have enough to retire if you are comfortable with your situation, expert says

Reviews and recommendations are unbiased and products are independently selected. Postmedia may earn an affiliate commission from purchases made through links on this page.

Article content

By Julie Cazzin with Allan Norman

Advertisement 2

Article content

Q: My wife Caroline is 61 years old, retired from her job in southern Ontario last year, and is now doing a little part-time work. I’m 63 and planned to retire from my consulting job at the end of this year, but I’m not sure I can afford to, given the extended downturn in the stock markets. My registered retirement savings plan (RRSP) has $210,000 and my tax-free savings account (TFSA) has $61,000. I also have $180,000 in my corporation, but this will increase to $250,000 by year-end. My wife has $200,000 in RRSPs and $50,000 in a TFSA as well as an indexed pension of $55,000 per year. Our home is worth about $1 million and our retirement income goal is about $90,000 per year after tax. Can I still retire at the end of this year? — Simon and Caroline

Article content

Article content

Advertisement 3

Article content

FP Answers: It seems there are a couple of issues here that require some thinking through: Do you have enough money to retire? And what is the best way to optimize your retirement income?

I hear your concern that retiring now may no longer be realistic with the markets being down. As you know, markets are going to move up and down throughout your retirement. Perhaps this is a sign that even if you mathematically have enough money, you don’t have enough to provide you with the assurance to draw on that money. Let’s work out the math part of the equation and see if that helps.

Simon, you have three different accounts from which you can draw an income or a combination of incomes: a RRSP, TFSA and your investment company (Investco), and they all have different tax characteristics.

Advertisement 4

Article content

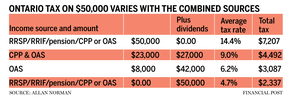

In the accompanying table, I have shown the average tax rate and total tax paid based on $50,000 income from differing sources.

Looking at the table, you can see the tax differential between non-eligible dividends and your other types of income. The question is, how to take advantage of the tax differences? What if you delay Canada Pension Plan (CPP) and Old Age Security (OAS) to age 70 and draw $50,000 in dividends until you deplete the Investco investments and close it up?

I don’t see an obvious reason for delaying withdrawals from your Investco. The costs of investing inside a corporation are an annual tax return and accounting fees. Plus, the taxable portions of interest, dividends and capital gains are taxed at about 50 per cent, although there is a refund mechanism that returns some of the tax when a dividend is paid out.

Advertisement 5

Article content

Deferring your OAS and CPP to age 70 means increasing them by 36 per cent and about 42 per cent, respectively. Combined, that is about $33,000 in today’s dollars and $40,000 in actual dollars compared to a CPP plus OAS payment of $29,000 in actual dollars if you started them at age 65. Delaying CPP and OAS until age 70 is worth about an extra $11,000 per year indexed for life.

I know some people are concerned that if they die early, they may not collect as much CPP or OAS and that is true. However, keep in mind, in this case, you are saving $5,000 per year in tax, and you are winding down your Investco once the investments are gone, saving you $1 to $2,000 in annual accounting fees.

The other reason you may not like my suggestion of delaying your CPP and OAS is the fear of spending money. It is nice to have some guaranteed income and I have clients who tell me they don’t want to draw much from their investments until their CPP and OAS starts. In your case, Caroline has a good base income for both of you, so this shouldn’t be a concern.

Advertisement 6

Article content

Now, what will mess up the suggestion of using dividends first and delaying CPP and OAS is Caroline’s pension income. It is likely that she will split some of her pension income with you, giving you some taxable income. But it doesn’t matter since there is still an advantage in drawing down from your Investco first.

-

Should we use TFSA savings to pay off our mortgage?

-

What are the next steps after paying off student debt?

-

How should a new widow best organize finances and investments?

After modelling this with prudent assumptions, I found that you will have no trouble retiring at the end of this year, and can spend $90,000 per year after tax, to age 100, and then leave an estate with an after-tax value of about $4 million. If you decide to start CPP and OAS at age 65, that means leaving an estate value of $3.8 million instead. It is when you and Caroline turn ages 83 and 81, respectively, when your net worth is larger by taking CPP and OAS at age 70 rather than 65.

Advertisement 7

Article content

Simon, you have enough to retire if you are comfortable with your situation. There are many ways to construct retirement income and the best plan today may not be the best plan when circumstances change. Don’t get too hung up on trying to find the most optimal plan, but rather focus on one that works and that you are comfortable with.

Allan Norman provides fee-only certified financial planning services through Atlantis Financial Inc. and provides investment advisory services through Aligned Capital Partners Inc., which is regulated by the Investment Industry Regulatory Organization of Canada. Allan can be reached at [email protected]

_____________________________________________________________

If you like this story, sign up for the FP Investor Newsletter.

_____________________________________________________________

{kind=link}

Comments

Postmedia is committed to maintaining a lively but civil forum for discussion and encourage all readers to share their views on our articles. Comments may take up to an hour for moderation before appearing on the site. We ask you to keep your comments relevant and respectful. We have enabled email notifications—you will now receive an email if you receive a reply to your comment, there is an update to a comment thread you follow or if a user you follow comments. Visit our Community Guidelines for more information and details on how to adjust your email settings.

Join the Conversation