This article is an on-site version of our Unhedged newsletter. Sign up here to get the newsletter sent straight to your inbox every weekday

Good morning. Goldman Sachs’ investor day yesterday failed to produce much excitement. The most interesting thing about Goldman is that it just isn’t that interesting any more, and its best strategic option is becoming still less interesting. That tells you something important about how the finance industry has changed. Email us: [email protected] and [email protected].

The housing recession, and the plain old recession

We check in on the housing market every few months, for a couple of reasons. Because something like two-thirds of Americans have a big chunk of their net worth tied up in the housing market, it tells you something about how a lot of people feel, financially — a feeling that factors into the performance of all other markets. Second, because the housing market is rate sensitive, the market tells you something about the transmission of monetary policy into the real economy, a crucial issue at the moment.

The housing market story always begins with mortgage rates, which have changed direction lately, following inflation expectations back up; see the blue line, below. This mirrors, in part, the increase in 10-year Treasury yields. But notice also the pink line, which is the spread between Treasury yields and mortgage rates. That spread, as Jack Macdowell of the residential credit specialist Palisades Group pointed out to us, is 130 bps higher than usual. This reflects expected rate volatility. When mortgage lenders think rates might move quickly, they build a buffer into their pricing:

When rates rise, housing affordability declines. Here, from Capital Economics’ Sam Hall, is a chart of US mortgage payments as a proportion of incomes. Houses were last this unaffordable in the mid-1980s.

Renting looks much more affordable by comparison (chart from Goldman, which calculates affordability slightly differently):

Higher rates are creating not a price crash, as one might expect, but a frozen market. Measured by the Zillow home value index, prices are off their August peak but are only down a modest 1 per cent:

Prices may be stable, but transactions are down, as both supply and demand feel the chill. On the demand side, mortgage rate sticker shock is scaring off would-be homebuyers, dragging down new mortgage applications. This year’s shortlived dip in rates did give applications a bump, but it hasn’t lasted:

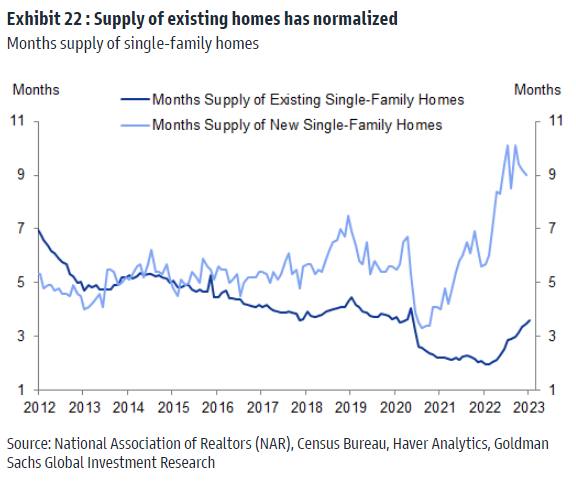

The dearth of willing buyers at current prices means that existing homes for sale just aren’t getting sold. Inventory is sitting around longer. The median single-family house listed on Zillow is more than two months old, the longest since early 2020. Contrast the rising stock of existing homes for sale — which accounts for about 90 per cent of home sales — against how many are actually being sold. The amount of existing homes on the market is back at pre-coronavirus pandemic levels (chart from Goldman):

Yet existing home sales (grey line below) are languishing at a fraction of 2019 levels. The chart below from Renaissance Macro shows both existing and pending home sales (pending tends to lead existing). Though pending home sales did jump in January, that probably reflects the fall in mortgage rates, which has reverted. Put together, existing home sales look a bit stuck:

The story is as much about supply as demand. High mortgage rates, which follow very low ones, create a lock-in effect. Homeowners (including one Rob Armstrong) cling on for dear life to their sub-3 per cent fixed-rate mortgages. It would take a lot to make them move. This limits how much of the existing home stock will come to market. A strong labour market also means few distressed sellers trying to dump their houses at a discount. Unless the economy craters (could happen!) the existing home market could be frozen for a while.

We should acknowledge here that the new homes market looks healthier. New homes sales are rising and, thanks to the pandemic building boom, more supply is coming online. Homebuilders, for their part, have no choice but to move inventory, and fast. According to Rick Palacios of John Burns Real Estate Consulting, they’ve cut prices, and those with mortgage lending offshoots are offering lower rates to get people in houses. Homebuilders may well steal market share as from the existing home market.

But, again, new homes only make up about 10 per cent of the market, probably too small to make a difference. As Goldman’s Vinay Viswanathan wrote recently:

Record-low homeowner vacancy rates have essentially depleted housing inventory and materially tightened supply. On net, this implies a muted impact from completions on the current supply/demand balance of housing and, ultimately, prices. Even if every single home under construction was completed and listed on the market immediately, the months’ supply of homes (the ratio of inventory to annual sales) would still be below historic averages.

So, what unfreezes the US housing market? Well, the easiest thaw would come from falling interest rates, which would restore affordability and help buyers and sellers meet in the middle. Another reason to hope the deflation fairy will appear soon, wand a-waving. But that might not happen, or happen soon.

How about a decline in prices? When rates first began to rise, the consensus among housing pundits (as far as we could make it out) was that while price increases would slow or stop, a price decline was unlikely. The argument was that substantial price declines are driven by forced sellers, and there won’t be many of these this time around, because there are so few adjustable-rate mortgages now (less than 8 per cent of the total), and because mortgage credit quality has improved since the financial crisis.

Now that rates have run as far as they have, more observers foresee only a smallish decrease in prices — 10 per cent or so down from the peak. This makes sense, provided we don’t get another big leg up in rates (a possibility we would not rule out). Supply is limited, and then there is the lock-in effect. This ain’t 2008.

But even if rates remain high, at some point the outlook for the economy should become a little clearer, and expected rate volatility should stabilise. At that point, the Treasury/mortgage rate spread should head back towards normal, supporting affordability. In combination with a modest decline in prices, this could cause a partial market thaw.

What does all this portend for the wider economy? There are two questions here. The first is simply how much lower housing activity drags on the economy. The second is more complicated: is housing just the part of the economy hit by higher rates first, with other parts of the economy following in time?

On the first question, Dhaval Joshi of BCA Research argues that the current housing recession will pull fixed investment in residential real estate down from about 4 per cent to 2 per cent of GDP, with something more than half of the damage already done. If that is right, lack of housing activity will be a perceptible, but not huge, drag on GDP. Joshi’s argument is that housing investment is quite cyclical, but reverts towards a level corresponding to the number of households in the country. We overshot that level the pandemic boom, and are now set to undershoot. His chart:

The question of whether the housing recession is just the first step in a rates-driven slump is harder. Joshi argues that since 1970, housing recessions (defined as a 1 per cent decline in housing investment’s contribution to GDP) have always been followed by general recessions. Housing is the “canary in the coal mine”, he says: it won’t drag us into recession, but it shows what high rates will do to the rest of the economy sooner or later.

We tend to agree. Other sectors of the economy are less sensitive to rates than housing. But if the economy is not cooling on its own — and it doesn’t look like it is — the Fed will have no choice but to tighten policy until what has happened in real estate happens elsewhere. (Armstrong & Wu)

One good read

That infamous slap seems to be helping Chris Rock’s career. Good for him!

{kind=link}